Finance leaders have always been expected to understand the numbers. That's the baseline. The harder and more valuable job is understanding the system that produces the numbers.

That distinction matters now because companies are more complex, more automated, and more dependent on cross-functional execution. AI is also moving quickly into finance workflows, including forecasting, reconciliations, close support, revenue recognition research, contract review, variance analysis, board reporting, cash forecasting, and scenario planning.

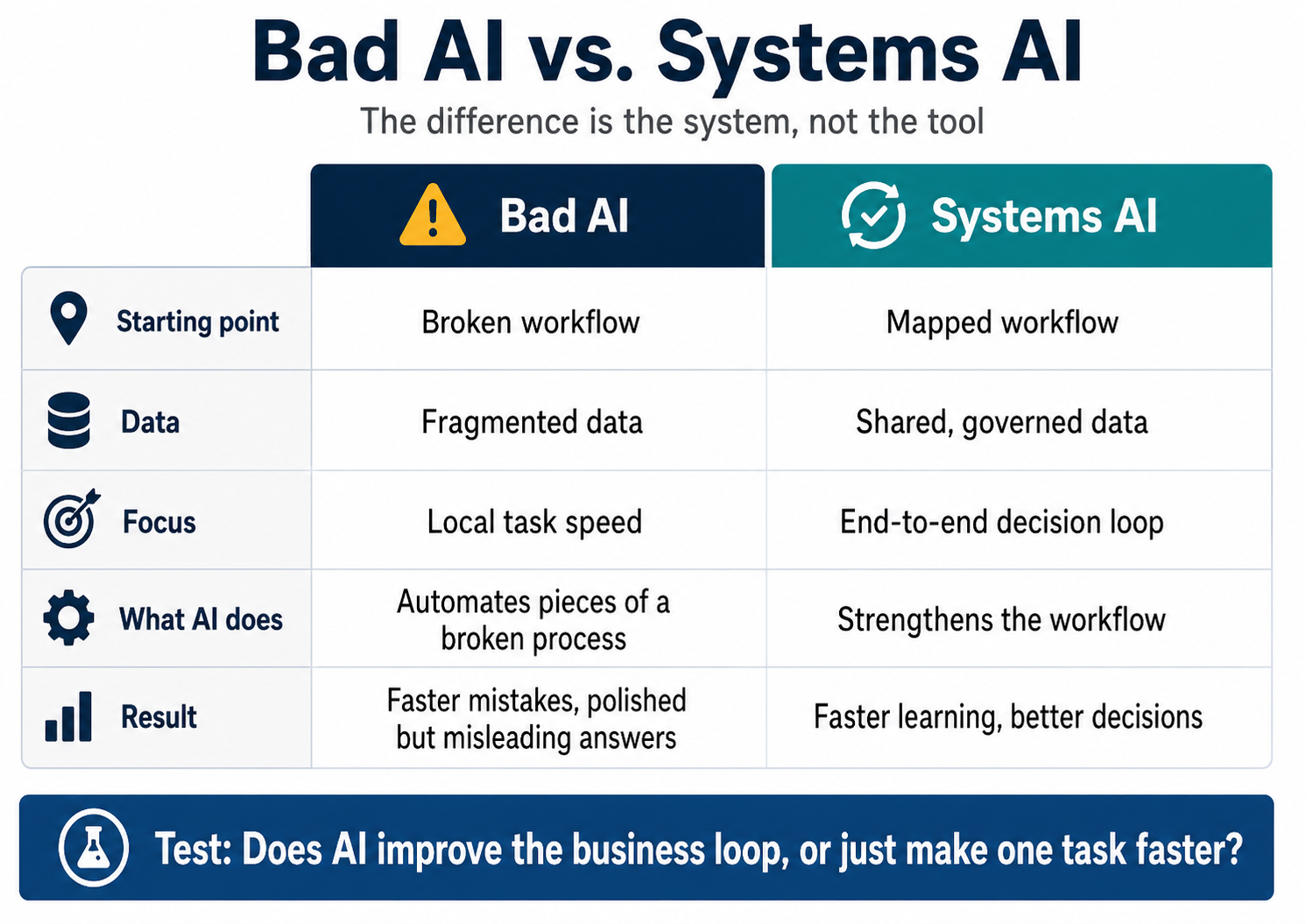

Used well, AI can make a strong finance and operating system faster and more adaptive. Used poorly, it can make a weak system fail faster. If the underlying workflow is fragmented, AI scales fragmentation. If the data is unreliable, AI produces polished but misleading answers. If incentives are misaligned, AI helps people optimize the wrong things more efficiently.

That's why systems thinking is becoming a core leadership capability for finance executives. The finance leader's job is no longer just to report what happened. It's to understand why it happened, how the pieces of the business interact, and what changes would help the company make better decisions. In the age of AI, finance leaders cannot simply automate the old machine. They have to understand and redesign the machine.

AI isn't just a finance productivity tool

Much of the AI discussion in finance focuses on task productivity. Can AI draft a variance explanation, summarize a contract, help with reconciliations, pull together accounting research, or create a first draft of a board slide? Yes, it can do many of those things, and used carefully, those gains matter. But task automation isn't transformation.

A finance team can use AI to make one analyst faster. That's useful, but the larger opportunity is to ask how the work itself should change. Should forecasting still work the same way if AI can synthesize pipeline commentary, historical conversion rates, customer behavior, macro assumptions, and operational capacity? Should revenue recognition review still follow the same manual path if AI can flag contract language, summarize exceptions, and point people toward the highest-risk judgments? Should project profitability analysis still wait until month-end if AI-enabled workflows can surface labor, scope, and pricing issues earlier?

The value isn't simply in doing finance work faster. The value is in helping the business learn faster. That's a systems question, not a software question.

What systems thinking means in finance

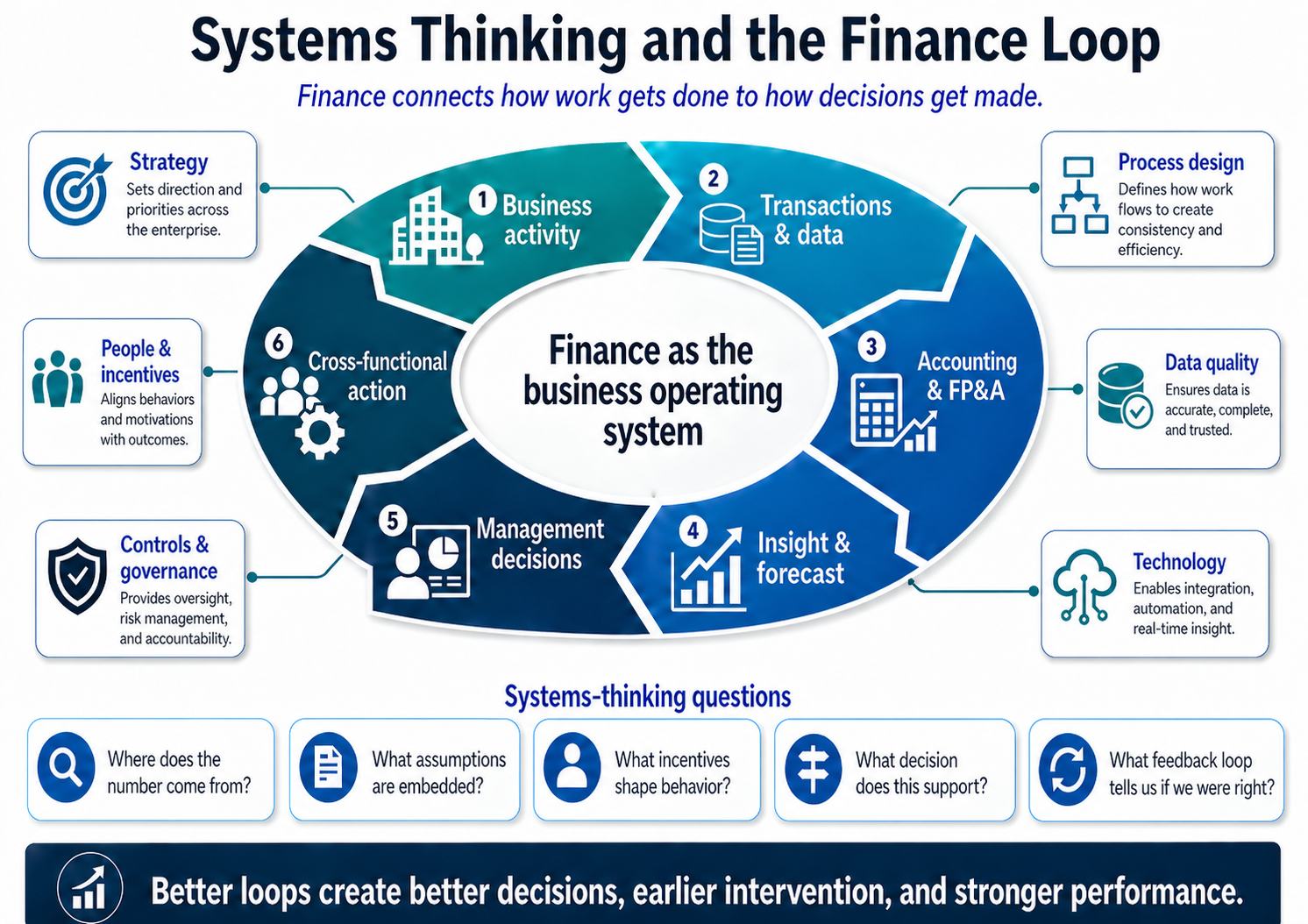

Systems thinking means looking at the whole, not just the parts. In finance, that means understanding how strategy, operating processes, data flows, incentives, technology, people, controls, and decisions interact. A financial result is rarely caused by one thing.

Margin compression may look like a pricing problem, but it may actually reflect sales incentives, delivery inefficiency, weak project scoping, resource constraints, product complexity, poor data, or several of those factors together. A missed forecast may look like an FP&A problem, and sometimes it is, but more often it's a sign that the company lacks a healthy feedback loop between sales, operations, finance, and leadership. A slow close may look like an accounting problem, but it may also point to bad upstream data, unclear ownership, disconnected systems, manual workarounds, or business processes that were never designed with financial reporting in mind.

Systems thinking asks practical questions: Where does this number come from? What assumptions are embedded in the process? What incentives shape behavior? What decision does this analysis support? What feedback loop tells us whether we were right?

Those questions separate finance teams that produce reports from finance teams that improve companies.

Finance sits at the intersection of the business

Modern companies run through systems: ERP, CRM, HRIS, billing platforms, project management tools, data warehouses, planning platforms, analytics dashboards, and now AI-enabled workflows. The financial truth of the company is distributed across all of them.

A revenue forecast depends on sales behavior, pipeline hygiene, customer expansion patterns, product usage, implementation capacity, churn risk, billing rules, and pricing discipline. Gross margin depends on product architecture, labor deployment, supply chain, project scoping, customer mix, contract structure, and operational execution. Cash flow depends not just on collections, but on contracting terms, invoicing accuracy, procurement behavior, hiring plans, and management discipline.

Finance sits at the intersection of these flows, which gives finance leaders a view of the whole company that most functions don't have. But seeing the whole company requires more than technical accounting or financial modeling skill. It requires curiosity about how work actually gets done.

This is also where finance has a special responsibility in AI adoption. Finance owns trust. Boards, investors, lenders, auditors, regulators, and management teams rely on finance to produce information that's not just fast, but reliable. That doesn't mean finance should block innovation. It means finance should help make innovation usable, governed, and connected to business decisions.

A real-world example: when finance becomes an operating system

One of the clearest examples from my own experience came in an organization where finance, operations, R&D project management, and resource scheduling were deeply connected, but the systems supporting them were not. At first glance, the project could have been described as an ERP implementation. That would have been too narrow.

The real issue was that the organization needed a better operating model. Project economics, labor allocation, resource scheduling, pricing, and financial reporting all needed to work together. If finance implemented software without understanding those connections, the company would have ended up with a cleaner database and the same management problems.

So the work had to start with the system. How did projects get priced? How was labor planned? How did managers know whether resources were being used profitably? How did operational activity become financial reporting? What did leadership need to know in order to accept, reject, or reprice work?

By integrating ERP with R&D project management and resource scheduling, and by building better labor cost visibility, the organization could manage project economics in a more disciplined way. The result was not just better reporting. It was better decision-making, better accountability, and better economics.

That's systems thinking in practice. A narrow finance lens asks, "How do we improve reporting?" A systems lens asks, "How do we make the business easier to run?" Those are very different questions.

Another example: crisis as a systems failure

Systems thinking also matters in crisis situations. Earlier in my career, I joined a public company in the AI and knowledge management space that was facing serious financial and government contracting challenges. The obvious issues were cash, compliance, and audit risk, but those were not isolated problems. They were symptoms of a broader system under stress.

Government contract accounting is a good test of whether a company understands its own economics. Labor categories, indirect rates, cost pools, billing practices, documentation, project management, compliance requirements, and cash flow are all connected. Weakness in one part of the system can create consequences elsewhere.

Fixing the problem required more than technical accounting. It required stabilizing the business, negotiating with government auditors, improving the cost model, strengthening reporting, and creating a clearer operating rhythm for management. That experience reinforced a lesson I have seen repeatedly: when a company is in trouble, the financial statements are usually the last place the problem appears. The real problem has been building inside the operating system for months or years.

Finance leaders who understand systems can intervene earlier because they can see weak signals before they become crises.

Where companies go wrong

Many companies try to solve systemic problems with local fixes. That's understandable, especially when the business is moving quickly and leadership wants visible action. The problem is that local fixes often make one part of the company look better while leaving the underlying system unchanged.

Consider three common examples. A sales team misses the number, so leadership changes the commission plan, but the real issue may be weak qualification, unclear customer segmentation, poor implementation capacity, or pricing that rewards bookings the company cannot deliver profitably. A close process runs late, so accounting adds more checklists, but the real issue may be bad upstream data, inconsistent ownership, or operational systems that were never designed to support financial reporting. A forecast misses repeatedly, so FP&A builds a more detailed model, but the real issue may be that sales, customer success, operations, and finance are not working from the same assumptions.

This is how companies end up with the appearance of discipline but not the substance of it. They create more reports, more meetings, more dashboards, and more controls, yet the business doesn't make better decisions. AI can make this worse if it's applied carelessly, because a company can automate pieces of a broken process and convince itself it has transformed. It hasn't transformed. It has only made the fragments move faster.

The real risk: losing judgment

AI can produce outputs that look clean, confident, and complete. That makes it tempting to trust the answer before understanding the system that produced it, which is dangerous in finance.

A model can be technically correct and still miss the business reality. A variance explanation can be well written and still avoid the real issue. A forecast can be sophisticated and still depend on weak assumptions. A dashboard can be attractive and still fail to change decisions.

AI doesn't eliminate the need for judgment. It raises the value of judgment. A finance leader still needs to ask whether the result makes sense, which assumptions are doing the heavy lifting, what could be missing, where the model breaks, and what the operating team would say if they saw the output.

Those are not clerical questions. They're leadership questions. The danger isn't that AI will replace finance judgment. The danger is that weak finance organizations will stop developing it.

Basic principles for finance leaders

Systems thinking doesn't require theory for its own sake. It requires a disciplined way of looking at the company. These principles are a practical starting point.

1. Start with the business outcome, not the finance output

A report isn't the outcome. A dashboard isn't the outcome. A forecast isn't the outcome. The outcome is a better decision.

Before building a model or automating a workflow, finance should ask what decision the work will support, who will use it, when they will use it, and what they will do differently because of it. If the answer is unclear, the work may still be interesting, but it's probably not valuable.

2. Follow the data upstream

Finance often receives data after the business has already shaped it. By the time a number appears in the general ledger, CRM, billing system, or planning model, many assumptions and behaviors have already influenced it.

Follow the data upstream. Where was it created? Who entered it? What incentives affected it? What definitions were used? What system transformations occurred along the way? Many financial problems are actually data lineage problems.

3. Look for feedback loops

Healthy companies learn quickly. Unhealthy companies repeat the same mistakes with better explanations. In finance, a feedback loop exists when information from results changes future behavior.

Project profitability analysis should influence pricing and scoping. Churn analysis should influence product, sales, and customer success. Forecast accuracy should influence pipeline management and operational planning. If analysis doesn't change behavior, it's not a feedback loop. It's a ritual.

4. Beware of delayed consequences

Systems often produce delayed effects. Hiring decisions made today may create cash pressure six months from now. Poor contract terms may not hurt margins until delivery begins. Weak implementation discipline may not show up until renewals decline. Underinvestment in finance systems may not be visible until the company tries to scale.

Finance leaders are valuable because they can connect present decisions to future consequences.

5. Design for accountability

A system without clear ownership becomes a blame machine. If a metric matters, someone must own the input, the process, the decision, and the follow-up.

AI doesn't remove accountability. It makes accountability more important, because automated workflows can obscure who made or approved a decision.

6. Make complexity visible, then simplify where possible

Modern businesses are complex. Pretending otherwise is dangerous. But complexity should be understood, not worshipped.

The goal isn't to build the most sophisticated model. The goal is to create enough clarity for better action. A good finance leader reduces unnecessary complexity while preserving the complexity that matters.

The CFO as system architect

The CFO role has expanded because the needs of the business have expanded. Finance leaders are expected to support growth, protect cash, improve decision-making, manage risk, digitize finance, strengthen controls, and help the company use data more intelligently. That's broader than "run finance."

It's closer to enterprise decision architecture. The best finance leaders are not trying to take over every function. They're trying to connect the company well enough so that better decisions become possible.

That means finance needs to understand sales without becoming sales, understand operations without becoming operations, understand product and engineering without pretending to be product or engineering, understand systems without confusing software with process, and understand AI without chasing novelty.

This is where finance can become one of the most valuable integrators in the company.

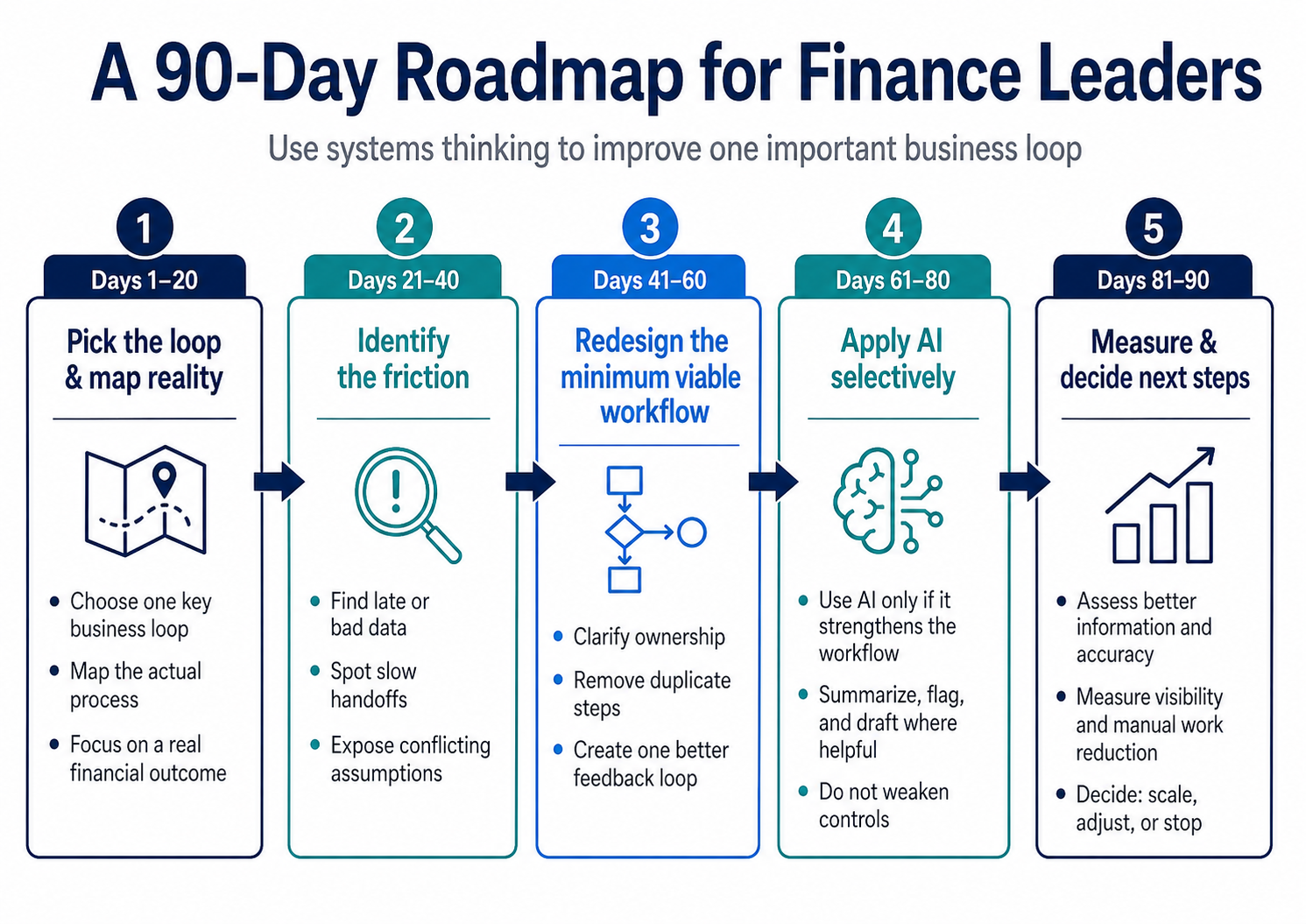

A realistic starting point: one business loop, 90 days

Systems thinking can sound abstract, so it helps to make it concrete. But finance leaders need to be honest about what's realistic. You're not going to redesign the company's operating system in 90 days. You're not going to fix every data problem, clean up every workflow, implement AI responsibly across finance, and change cross-functional behavior while still closing the books, supporting the board, managing cash, and handling the daily fire drills.

That's not how real companies work. What you can do in 90 days is prove the method.

Pick one important business loop where better information and faster learning would improve decisions. Good candidates include project profitability, forecast accuracy, working capital, pricing discipline, revenue recognition support, customer profitability, or headcount planning. The goal isn't transformation theater. The goal is one visible improvement that makes the business easier to understand and easier to run.

Days 1–20: Pick the loop and map reality

Start with one financial outcome that matters. Don't begin with the report. Begin with the work.

If the issue is project profitability, map how projects are sold, scoped, staffed, executed, tracked, billed, reviewed, and repriced. If the issue is forecast accuracy, map how pipeline information is created, updated, challenged, converted into assumptions, and reviewed by leadership. The key is to map reality, not the official process. Every company has a formal process and an actual process. Finance needs to understand the actual one.

Days 21–40: Identify the friction

Look for the places where the system breaks down. Where does data enter late or incorrectly? Where do teams use different versions of the truth? Where do handoffs slow down? Where does finance receive information after the decision window has closed? Where are people optimizing their own department at the expense of the company?

This phase doesn't require a giant transformation office. It requires structured conversations, process observation, data review, and a willingness to ask basic questions without assuming the answer.

Days 41–60: Redesign the minimum viable workflow

Don't automate yet. First, redesign the smallest part of the workflow that would create meaningful improvement.

Clarify ownership. Standardize one or two key definitions. Remove duplicate steps. Improve one data handoff. Change the timing of one review meeting. Make one decision right explicit. Create one better feedback loop. This is where practical systems thinking differs from abstract systems thinking. You're not trying to solve everything. You're trying to remove enough friction that the system performs better.

Days 61–80: Apply AI selectively, if it helps the system

Only now should AI enter the conversation. Use AI where it strengthens the redesigned workflow, not where it merely makes finance look modern.

That might mean summarizing contract terms, flagging anomalies in project costs, drafting variance explanations, accelerating revenue recognition research, synthesizing forecast commentary, or creating scenario narratives for leadership. But the test should be simple: does this improve the business loop, or does it merely make one task faster?

If it weakens controls, creates confusion, or shifts work onto another department, it's not progress.

Days 81–90: Measure, govern, and decide what comes next

At the end of 90 days, don't declare victory. Assess what changed. Did managers get better information earlier? Did forecast accuracy improve? Did margin leakage become more visible? Did finance reduce manual work without weakening controls? Did the pilot reveal a larger systems issue that needs executive attention?

The output of the first 90 days should be a clear decision: scale, adjust, or stop. That's a realistic ambition. Not "we transformed finance in 90 days," but "we proved that systems thinking can improve one important operating loop, and now we know where to go next."

The mindset shift

The most effective finance leaders I have worked with are not just technically strong. They're integrators. They understand accounting, but they're not trapped inside accounting. They understand systems, but they don't confuse software with process. They understand AI, but they don't chase novelty. They understand controls, but they also understand speed. They understand the boardroom, but they stay close enough to operations to know how the business actually works.

That combination is increasingly valuable. Finance leaders have an opportunity to become architects of better operating systems inside their companies, not by taking over other functions, but by connecting them. The goal isn't to produce more reports. It's to improve the way information becomes action. The goal isn't to use AI to make finance look modern. It's to use AI to help the company learn faster and make better decisions.

Systems thinking isn't a buzzword. It's a practical leadership discipline. It's how finance moves from explaining the past to improving the future. And in the age of AI, that may be the most important shift of all.